Why I'm entering the Crowdfunded Space

And why you may want to also...

“The conventional approach to investing for retirement was 60% equities and 40% bonds. If your goal was 10% a year this mix got the job done in the 80s, 90s and 00s. Not anymore... Now, bonds return zero. So does 40 go to zero with it? What do we replace bonds with?

One idea could be to increase exposure to alternative assets. Crypto, cars, art, baseball cards, etc Most people have 0-5% in alts. This allocation will probably change if bonds remain at 0...it’s just the math. “

— Chamath Palihapitiya via Twitter

If you’ve noticed the recent IPO market, one thing you’ll notice is that the game is rigged against retail investors. Take $SNOW for instance. At the open the stock surged to nearly $320 per share. It’s currently at $240 per share. Think about that. If you were a retail investor who wanted to buy in early, it’s a possibility that you’ve already suffered a 25% drawdown on your investment. Which means you need the stock price to go up 33% from it’s current levels just to breakeven. This type of story is one of the biggest problems facing today’s market.

One of the biggest sells that brokerages and finance companies use to pitch the idea of stock investing is the story of Microsoft or Apple. If you invested $10,000 in these companies at start up your investment would now be worth X million dollars. While this story is true, the story doesn’t tell you the whole truth about these companies.

Let’s look at the story of $GOOG to give us a better idea of how IPOs have changed in recent years. $GOOG went public in 2004. At the time it’s market cap was a whopping $23 billion dollars. However looking at it’s financials, it’s market cap was hardly speculative. On it’s filings prior to the IPO, $GOOG was already a profitable company. In the TTM leading up to the IPO it’s net income was close to 200M dollars, it’s Revenues were over 2B dollars. In other words it went to market with a PE ratio of 100, a P/S ratio of 10 and it’s revenue growth was over 100% YOY.

By comparison $SNOW went public at a TTM Price to Sales ratio of 82.4! If we applied this same ratio to $GOOG, it’s IPO valuation would have been $190B! This would have made it one of the 10 largest companies in the world by valuation on it’s IPO date!

VC re-wrote the rules

You could argue the playbook for IPOs changed with the $FB IPO in 2012. When they went public, the company went public at a valuation of $104B! 5x the valuation of $GOOG. Why the difference in valuation?

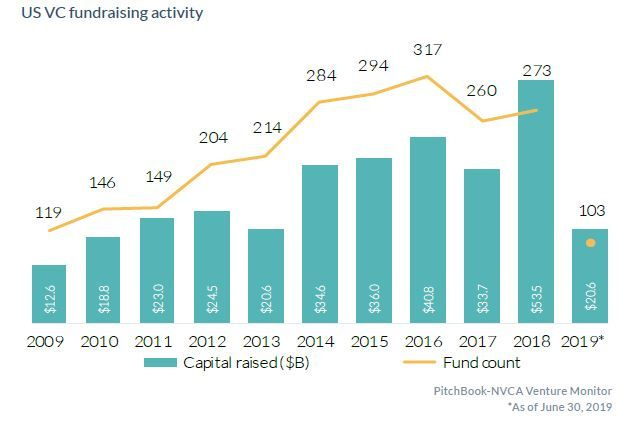

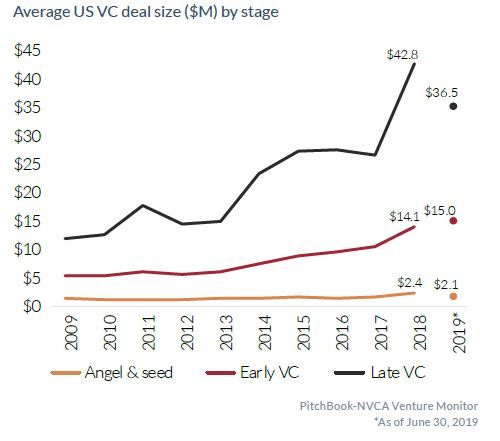

Take a look at these two charts from pitchbook.com

21 Charts Showing Current Trends in US Venture Capital

One change has been the rise in VC fundraising. Notice that capital raised has nearly tripled in the past 10 years (chart US VC Fundraising Activity). However notice in chart 2 (Average US VC deal size by stage) at what stage that VC is piling in at. Late stage VC. Notice the trend started to really accelerate in 2013. In May of 2012 Facebook had its IPO. Since that time more and more venture capitalists are pouring money into late stage companies in an effort to keep them private longer and allow them to grow more before going public. As a result companies that are labeled more ‘mature’ are coming to market. However are these companies really more ‘mature?’

Judging by profitability, no they are not. They are still immature companies which are not turning a profit. However the market’s valuation at IPO is more mature because it’s relative to the fixed valuation already set by the private market. In other words if the private market said it was worth 15B in the last round of fundraising, and revenues are growing 100%, it may then be priced at 25B for the IPO. By the time it hits the retail market, the valuation may well be at 35B once the institutional investors get their hands on it. When retail gets in, institutional investors tend to get out. Retail is left holding the drawdown. Once lock up expires, VC and Angels can cut back, leaving Retail holding an even bigger drawdown. Even assuming the company one day hits a 100B valuation, the rewards premium is only 3x the price. Still a fair reward, but paltry compared to the 50x growth of $GOOG or even the 2000x return of an $AAPL or $MSFT.

The Government re-wrote the rules

To get the returns of an $AAPL or $MSFT you have to be able to invest in companies when they are valued under $1B. An investment in a $20M company could return 100, or 1000x the investment if it grows to $20B or $200B. Unfortunately few public companies are capable of this type of growth and until recently only the elite had access to the private markets.

In 2012 as a result of the Jumpstart Our Business Startups Act (JOBS), the US government opened the door for non accredited investors (the majority of retail investors) to begin investing in startup businesses. A part of this act was the Regulation CF (Crowd Funding). It allowed private companies to raise limited amounts of capital from all American investors.

Perhaps no company better illustrates the potential and the perils of Crowdfunding than Zenefits. The company once valued at 4.5B by Andreseesen Horowitz, got some of its initial backing from Crowdfunding site Wefunder. At the time, investors were looking at unrealized gains of up to 4,000%. The return multiple given on the site was 286x the initial investment!

Of course whether Zenefits ever makes it to the market or is acquired is still a question left to answer. Investors may never realize a return on their investment, unless a secondary market exists which allows them to sell their shares in the company. The crowdfunding site StartEngine is currently working on such a market and expects to open it via end of fiscal year (note I do have an invested interest in StartEngine). Could this be the start of a much needed movement to liquidity which sparks the rush in? Maybe. It’s certainly worth watching.

Equity is not the only option for investing in the Crowdfunded space. There also exists sites like Groundfloor which allow for real estate crowdfunding. RichUncles allows for REIT crowdfunding. Debt funding exists, Farm funding, etc.

On these different sites like Republic, StartEngine, MicroVentures, etc. there are companies raising capital for ventures like payday loan crowd funding (Hundy), alt assets IRA (altoIRA), and other platforms which attempt to decentralize the access to valuable assets.

This decentralization of alternative assets once only available to the mega rich inevitably will hit speed bumps. However with minimums as little as $20-$50 dollars, the ability to diversify will give investors an opportunity to pursue a big return with manageable risks. The loss of investment is real, but so is the opportunity to make a 20x return. I believe its worth a risk to keep a small amount (1-2% max for startups, 2-5% for debt/real estate) and will be slowly moving some of my assets over to these platforms. If you think the stock market is looking overcrowded, maybe you should think about it too.