Probabilistic thinking...when and how you should bet against the market.

Not very often.

You may have heard the stock market goes up about 70% of the time. Have you ever wondered how they got that number?

It’s based on annual returns. Yet there is a flaw in this mechanism. Not everyone invests money on Jan 1 with the expectation of withdrawing on Jan 1 the year after. When looking at returns, I thought it might be worthwhile to look at data across multiple time frames, and measured not at the start of each year, but at the start of each month.

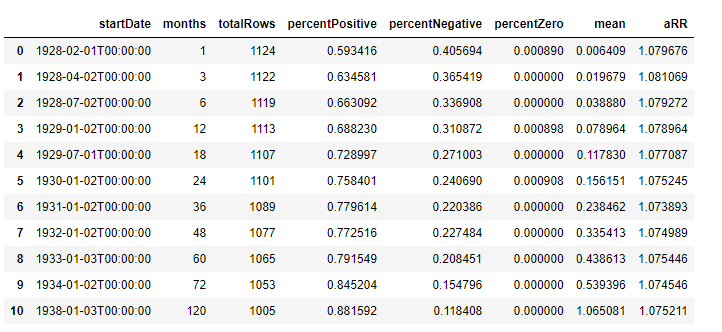

I gathered data from 1928 for the S&P 500. I charted all of the results measuring from the start of each calendar month on a monthly, quarterly, semiannual, annual basis, 18 months, etc… up to 10 years. I wanted to share the results:

Months is the time frame measured (monthly, quarterly, etc.)

Total Rows is the number of data points measured

% Positive/Negative/Zero is just that, what % of the returns were above/below/equal to zero.

Mean is the mean percentage of return over the data set.

ARR is Annual Rate of Return (as calculated by using the CAGR formula).

Now going back to the title…Probabilistic Thinking, When and How You Should Bet Against the Market?

Data says…not often.

If you follow me, it’s possible that like me you are a contrarian. This means that when the market is bullish, you are likely bearish. It also means you will likely be bearish more often than you are bullish. That being said, you must fight your contrarian instincts and understand that more often than not, it pays to follow the crowd.

However irrational and illogical as the market may seem, statistically, history favors the bulls. So if you want to bet bearish, you’d better be extremely confident in your thesis, and you’d better calibrate your confidence properly.

That being said there is something to be learned for bearish bets in this data…

The shorter, the better.

It seems counterintuitive to believe that time is the enemy of a well crafted bear thesis. After all isn’t the market a weighing machine over the long term? For stocks yes, for indexes no. Indexes change the rules. They kick out laggards and add in up and comers. They diversify sectors and risks. Which is why it’s entirely stupid that the market’s way of hedging risks is with SP500 puts…a bet that is guaranteed to fail over time.

Major depressions and recessions in modern history have happened only 3 times in the past 100 years. Each lasted between 18-36 months each time.

Let’s assume you see a bubble forming and predict a potential 50% downside to the market, given the historical data, you should only apply between around a 3% likelihood of it happening.

Even if you add up the time of those major crashes (72 months), plus add a month in for the COVID crash, Flash Crash and Black Monday. That’s 75 months in a data set of 1100 months or about 7%.

At those odds, statistics say your average expected loss would be 3-4% in such a scenario. Over a 1-6 month horizon, avoiding a 3-4% loss is significant…but over a year or more, you should assume the risk of a 3-4% loss for the expected historical average of 8% returns.

Of course this isn’t to say that you can’t spot a bubble. Bubble’s are often seen. Predicting it’s burst is much harder, and that’s why it’s foolish to take a long term short bet against the markets.

It’s far more rewarding to act when the bubble is bursting.

Take a look at this data below:

I’ve included biggestGain and biggestLost columns, biggestLost being the largest drawdown on record in the data set. As you can see in one month, the market historically has given up as much as 30%. The largest three month drawdown was 46%, for a six month period, 53%.

But when compared to the largest gains, one month bearish bets have a much better hit rate, and much less downside 1.5-1 (max upside vs max drawdown for one month scenarios) as opposed to nearly 2-1 of worse in three months or longer.

So if you feel tempted to time the market, or if you are very bearish and trying to figure out how to position…here are some takeaways that may help you.

Statistically the biggest payout, and the most probability of success for bearish bets come from short term bets.

Before I go, one more thing….it’s worth mentioning that the previous data set includes numbers from what appears to be a bygone era. The idea of interest rates above 4% is a foreign concept to those who don’t remember life before the internet.

How do these statistical lessons hold up since the end of the Great Financial Crisis?

Here is the data:

The data skews even more bullish then normal. While short term bearish hedges have a higher hit rate then any longer term, compared to the historical norm it’s about 20% less than the historical averages. Thus, probabilistically you have to factor that in when thinking about a bearish bet.

So what’s the lesson — It pays to be bullish, but if you must be bearish…be quick about it.