Pinterest -- Deep Dive

Hey everyone,

Thanks for taking a look at my deep dive into Pinterest. We’re going to break this article up into a few key sections: History, Business Model, Metrics, Financials, Management, Stock and then close off with my beliefs after my deep look into Pinterest.

Before I get started, let me explain what got me interested in Pinterest in the first place. Two years ago I was planning out how I would propose to my wife. I turned to Pinterest for proposal ideas. Then I came to Pinterest to help me find a wedding ring (it led me to Etsy, another one of my conviction investment ideas). After finding my vendor on Pinterest and buying a ring from her on Etsy, I found myself and my fiancee using Pinterest to plan out ideas for our wedding over the next 6 months.

At that point I realized the power of the platform. Every time I needed inspiration or an idea I went to Pinterest. Sometimes I would buy things, other times I would simply get an idea. I then realized that the platform was an advertisers dream. A platform where hundreds of millions of users come to look for inspiration and possibly even make a financial decision based on what they see.

While Pinterest is a social media platform, it’s differentiated from Snapchat, Instagram, Facebook and Twitter. On those platforms you go to share your photos, your viewpoints, your life and to interact with others. You are sharing yourself. On Pinterest you come to find projects, products and ideas and interact with them. You aren’t going really to share. You go to find.

This leads to more positive interactions, at the loss of the social element that other social media platforms have. The downside is that a user is not going to frequent Pinterest the way they frequent Snapchat, Instagram or Twitter. The upside is that a user who consistently finds inspiration will return to the platform after what is almost always a positive experience.

History

Pinterest was founded in December 2009 by Ben Silbermann, Paul Sciarra and Evan Sharp. A prototype of the site was launched in March of 2010. Nine months after the launch, the site was at 10,000 users. In 2011, Time listed Pinterest as one of it’s 50 best websites of the year. By the end of the year it was having 11 million unique visits weekly. It was the fastest site ever to break the 10 million mark.

Business Model

Over time Pinterest began to monetize it’s platform by giving businesses the opportunity to create accounts and to begin to Promote Pins. These Pins can be used to generate brand awareness, brand engagement or link directly to an e-commerce website.

For users the platform is completely free. Advertisers pay for promotion based on certain specific metrics.

The advertising platform for Pinterest is robust. It gives deep analytics into who is engaging with the business and offers advanced reports about the efficacy of different ad campaigns. As you can see below I’ve used Pinterest for a business account and must admit, I had some difficulty using all of it’s functionality. This is something that over time I hope the platform is able to address if they want to target small and medium businesses more effectively. However it may be designed by choice to concentrate on larger businesses first.

Pinterest sells its ad space on an auction based method. Depending on the objective of your ad, you may pay for either visibility, engagement or clicks. This is common among social media networks. It also gives Pinterest the same flywheel like effect. The key is to continue to increase users and user engagement. That brings more advertisers which then pushes ad prices higher and allows Pinterest to reinvest in getting more users.

Metrics

For Pinterest some of the key metrics are it’s Monthly Active User counts, both US and International.

In it’s most recent quarter Pinterest reported Monthly Active Users at 442 million. Of which 98 million are in the US and 343 million are international.

Here’s a look at Monthly Active Users historically:

Looking at the more recent numbers versus historical, you can see that the pandemic accelerated the companies monthly active user growth. It remains to be seen if this trend continues after the Pandemic. However management noticed that most of the growth was from the under 25 generation.

In looking at the latest trends on Pinterest, it seems likely that this generation is continuing to engage with Pinterest even after the initial surge. Currently fashion and outfit ideas are routing among the highest trending searches on the platform:

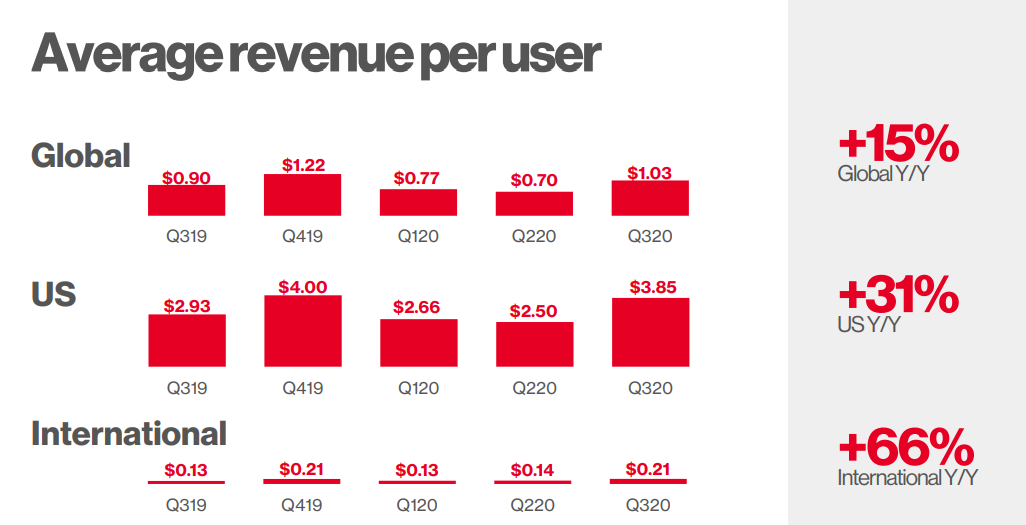

Another key metric for the company is Average Revenue Per User:

There is high levels of seasonality in Pinterest’s advertising revenues. Consistent with it’s high level of desirability for retail in the holiday seasons. However what’s interesting is the massive jump in Q3 revenues this year. Simply put it was the best quarter in history for Pinterest and now the company is heading into the seasonally strongest Q4.

It’s also worth noting that the US generates significantly more revenue per user than international. 20x more revenue per user. It remains to be seen how successfully Pinterest can monetize international users. However in the prior quarter international revenues per user grew 60% YOY. This suggests that there is still plenty of opportunity to increase ARPU in the international field.

Financials

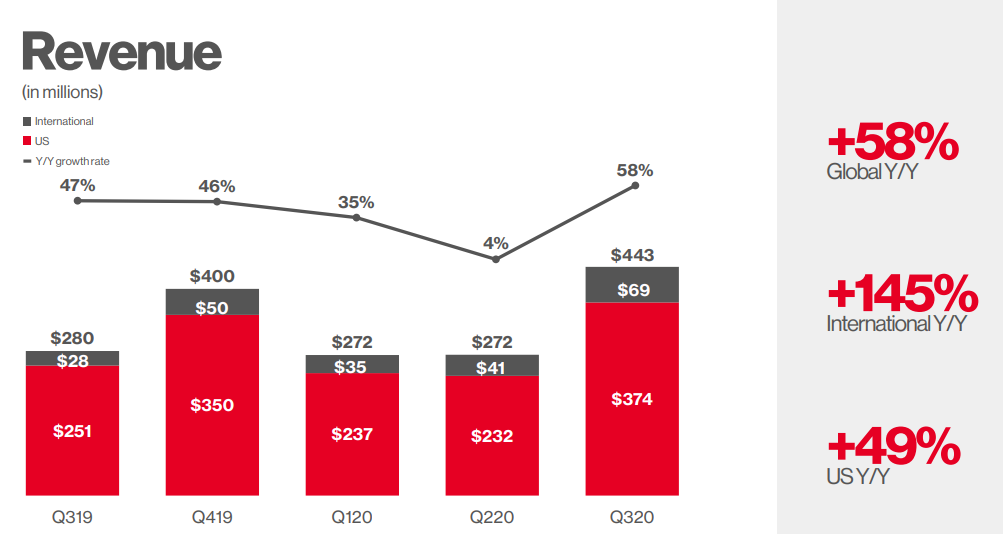

Pinterest is not a profitable company, however it is growing Revenues and reinvesting heavily into it’s business. Here are it’s revenues for the past 5 quarters along with YOY growth rates.

And it’s Non GAAP expenses over the same time frame. Note I emphasize Non GAAP. Later on I’ll hit on why that’s important:

And here are it’s quarterly revenues since 2016. As you can see, the company has significant seasonality and US revenue is much stronger than International revenue.

Finally a look at yearly GAAP financials for the past 3 years:

Management

Pinterest is a founder led company. Benjamin Silbermann is the Chairman, President and CEO. Co-Founder Evan Sharp is the Chief Design and Creative Officer. Benjamin went to school at Yale. Before Pinterest he worked for Google. Evan Sharp studied architecture at Columbia and graduated from Chicago. He worked with Facebook before co-founding Pinterest. Todd Morgenfield the CFO, has an MBA from Stanford. The board has a diverse background with highly relevant experience. I also appreciated this tidbit from their proxy statement:

One thing worth watching is the executive salaries. Being that they IPO’d the Proxy showed one time compensation figures which included special stock based compensation due to the IPO. It remains to be seen what the co-founders will take on an annual basis.

Stock

Currently there are about 600 million shares outstanding. Dilution is a real potential issue with this stock. The company has stated that they will recognize $635 million of future stock based compensation expense over the next 4 years. Currently they have over 700 million potential diluted shares outstanding. That’s over 15% potential dilution excluding future stock based compensation.

Looking at volatility the stock has a historical median draw down of 2.2% daily. I measured it by looking at the low relative to the open every day since it’s IPO. It has a standard deviation of 2.15%.

I share these numbers because they give you an idea of the volatility you can expect if you own Pinterest. It’s within normal distribution to see one day drops of 4%. When you really should start to look is if you see a one day drop of more than 8%. If you see the stock down 14% over a 2 day period or 17% over a 3 day period. Price movements of these magnitude should be analyzed to see whether a real buying opportunity is presenting itself, or whether the market believes that something fundamentally has changed about the business.

Concluding Comments

On a fundamental basis, Pinterest’s share price is getting a little rich at the moment. However looking into the inners of the business, it still has significant growth opportunities which I feel outweigh the downside risk. I do have some concerns about the business in the short term, and I’d expect to see some volatility, particularly after Q4. It’s currently priced at nearly 30x sales, shares are diluting quickly, and the company is still not Free Cash Flow positive. I also wish management would be more transparent about engagement stats as these are the real metrics that investors and advertisers want to know about. They certainly have the data and could share it if they wanted to.

However the revenue growth has been consistent and is accelerating. The pandemic is opening up new users to Pinterest for recipes, DIY projects and outlets for their creativity. These new users may come back to Pinterest for other events, even after the pandemic — Party Ideas, Wedding Plans, Gift Ideas. Advertisers and Retailers are likely to put significant ad spend on the platform in Q4. SquareSpace, Home Depot, Publix, Honeybaked, Havertys, Art of Shaving, Bank of America, Target, Walmart are all some of the advertisers that are using Pinterest right now. One of the great things for investors is that you can logon and see who’s advertising at any time.

Before we wrap up I wanted to highlight a few future growth areas for Pinterest. AR, Stories and Catalogs. Let’s start with one example of AR use. Pinterest is implementing the ability to try makeup on using AR. Considering how many users go to Pinterest for outfit ideas and looks, this is a compelling opportunity for Pinterest to drive engagement and of course, ad dollars. Not just in make up but in outfits, shoes, jewelry, etc.

Stories is another function that Pinterest is starting to roll out. I could get a gif so I have to link to a sample story.

Similar to Instagram Stories, Pinterest will allow users to tell a story about a product, place or idea via multiple pins that carousel as part of a larger story (they do offer carousel pins now, but it looks like Stories will give them advertisers some unique tools, like video). Some use cases that come to mind — a recipe broken down step by step, a travel destination in itineraries, a cruise package with breakdowns of each port. This is another compelling opportunity for Pinterest to drive ad sales by allowing businesses to have new tools to work with.

However what I feel the biggest revenue driver will be in the future is Catalogs. Pinterest is now allowing retailers to mass import catalogs of their products directly onto the platform in the form of pins which then link to the website.

These catalogs are pins with meta tags embedded in the links which allows Pinterest to track the click throughs to the retailer’s website. In each of the past earnings calls and shareholders letter, this catalog functionality has been referenced. It is clearly a big part of Pinterest’s future business plans. While in Q3 they didn’t give specifics regarding numbers, in Q2 they stated that sequential growth in catalog uploads from Q1 was 350%!

At the moment to the best of my understanding, Pinterest monetizes catalogs only when these are parts of an active ad campaign. So if a retailer is advertising a pin which is part of a catalog, and I click on it, then Pinterest would register a cost per click fee for the advertiser. However if the pin is not being actively advertised, a click would not generate revenue for Pinterest.

I suspect that at some point they will begin to charge a small fee for click throughs on all items in a catalog, even if these are not being promoted. This would seem a logical and unobjectionable practice. If you are selling a product and Pinterest is putting people in the door, will you really balk at paying a small fee for the lead? I suppose it depends on the price you are paying, and the price of what you are selling. However since Pinterest pays hosting fees for each of these items, it’s fair for them to expect some compensation. Also such a practice would limit a flooding of items into Pinterest’s ecosystem and oversaturating users with products which would devalue the effectiveness of paying ads. For a business with 100s or 1000s of SKUs being able to mass import your entire inventory to Pinterest at no cost is a bargain no matter how you slice it. It’s in essence a free extension of your e-commerce website with no hosting costs. Only a fee per use.

Another driver of Pinterest’s future growth is what’s going on at other social media websites like Facebook, YouTube and Twitter. Some advertisers are tiring of the negative press constantly around these platforms and in the case of Facebook, the perceived or real enabling of violent and extreme political groups. Pinterest is seen as not being an advertising space with negativity attached to it. Regardless for Pinterest to continue to grow revenues, catalogs is likely going to be the key driver.

Final Thesis

I expect User Growth to continue for the next 5 years as more millennials and Gen Z begin to use the platform for ideas and inspirations for some of life’s big events like graduation parties, dorm room ideas, study hacks, weddings, anniversaries, decorating their first home, etc. I would expect total users to range from 600M to 750M by 2025. I believe ad ARPU will continue to grow on a yearly basis by about $1 per year. This brings me to about $8.73 per user in ad revs per user by 2025. This would equate to revenues between 5.2B and 6.5B. I’m baking AR, Stories and Promoted Pins from Catalogs into these assumptions, but excluding non promoted pins from Catalogs. With a 10x P/S ratio, that would lead to a market cap of 52B to 65B.

Now let’s discuss Catalogs a little bit. I believe that at some point Catalogs will be monetized not just on an ad basis, but on a general basis. In other words I believe businesses will eventually have to pay for the privilege of posting their product catalogs on Pinterest. My assumption is that this will happen through click throughs. By 2025 I could see this making up 10% of total revenues. This would mean around 600M generated in catalogs.

The question is how much would businesses pay for click throughs to a product page and how many click throughs can Pinterest generate? I’ll work through a few assumptions. Assuming 675M monthly active users and these click through 1 catalog product per month, that would be roughly 8B click throughs in a year. Assuming that 80% of these click throughs are not promoted pins, that would leave 6.5B click throughs on non promoted pins. Would a business be willing to pay .10 per click through? I think most would without hesitation.

If you add this into total revenues that would lead to annual revenues of 5.8B to 7.1B. Again using a 10x P/S ratio, you’d end up with a market cap of between 58B to 71B.

So you can certainly see that I’m still bullish on Pinterest’s future revenue growths. However, I am watching closely to make sure share dilution slows post-IPO. Also I’ll be listening carefully for management to give more clues as to how they will continue to expand the use of AR, Stories and Catalogs. Finally of course I’m watching MAUs and ARPUs to make sure these continue to accelerate. Heading into the 4th quarter I’m expecting big jumps in both. However 1Q 2021 I would expect both to possibly contract. I could see the stock seeing a pullback in this quarter. I don’t view Pinterest as being purely a pandemic play, because after the Pandemic, event planning, travel and other outdoor activities likely will get users going back to Pinterest seeking ideas and inspiration.

Finally I’m curious to see how Pinterest finds other ways to generate revenues in the future. I suspect that travel and local restaurants will be big targets post-pandemic. Particularly the use of Stories would give them some monetization opportunities in these spaces. A local restaurant could pay to promote it’s story to users within a metro area that are looking at recipe ideas. Each page in the story could show step by step how a signature dish is made, or possibly each page could be a picture and description of a different signature item. A link to make a reservation could appear at the end of the story.

Travel companies like Expedia or Bookings could pay to promote stories for users looking at honeymoon or vacation ideas, and create a whole story for a specific locations or a story of different locations and link to a search or an offer on the website.

In conclusion, I think Pinterest is on the right track for growing monetization. I still see it as early innings. Long term I see the companies net worth being somewhere between 40-80B depending on market conditions by 2025. It’s a company I’m invested in and will stay invested in unless the fundamentals behind the company change significantly over the next 5 years. Hopefully this research helps you make a more informed decision or at least gives you more conviction one way or another about your own personal decision regarding Pinterest. Please don’t take it as financial advise as I’m not your financial adviser and not qualified to make investment decisions for you and your personal circumstances.