INTU - An overlooked TAM opportunity

If you are like me, you probably are starting to feel that the market is oversaturated with XaaS (as a service) companies. You have SaaS (Software), PaaS (Platform), IaaS (Infrastructure), UCaaS (Unified Communications), DaaS (Data), DBaaS (Database), etc.

Almost everything is an XaaS company at the moment and their is a reason for this. Subscription based service companies are often good at establish recurring revenue, creating sticky platforms to retain revenues, and expand multiple products on users over time to grow revenues.

However with so many companies offering subscription models, and especially cloud based subscription models, the problem is that it’s difficult for any one provider of a service to truly develop moats with things such as network effects. Especially when providers have also set up ways to transition users from one platform/software/database to another in a short time frame.

Over the past few weeks, I’ve been searching smaller cap companies to try and find if any of them are truly standing out by offering some sort of service which either has a reasonable valuation or has something that truly differentiates itself meaningfully from other vendors.

In doing my screens initially I landed on Bill.com ($BILL) an AP/AR cloud based platform with integrations to Intuit’s Quickbooks. I thought this was a promising idea. I decided to do some research, but my research led me to a company who I believe is even more promising albeit at a much larger market cap…Intuit (INTU)

Why Intuit?

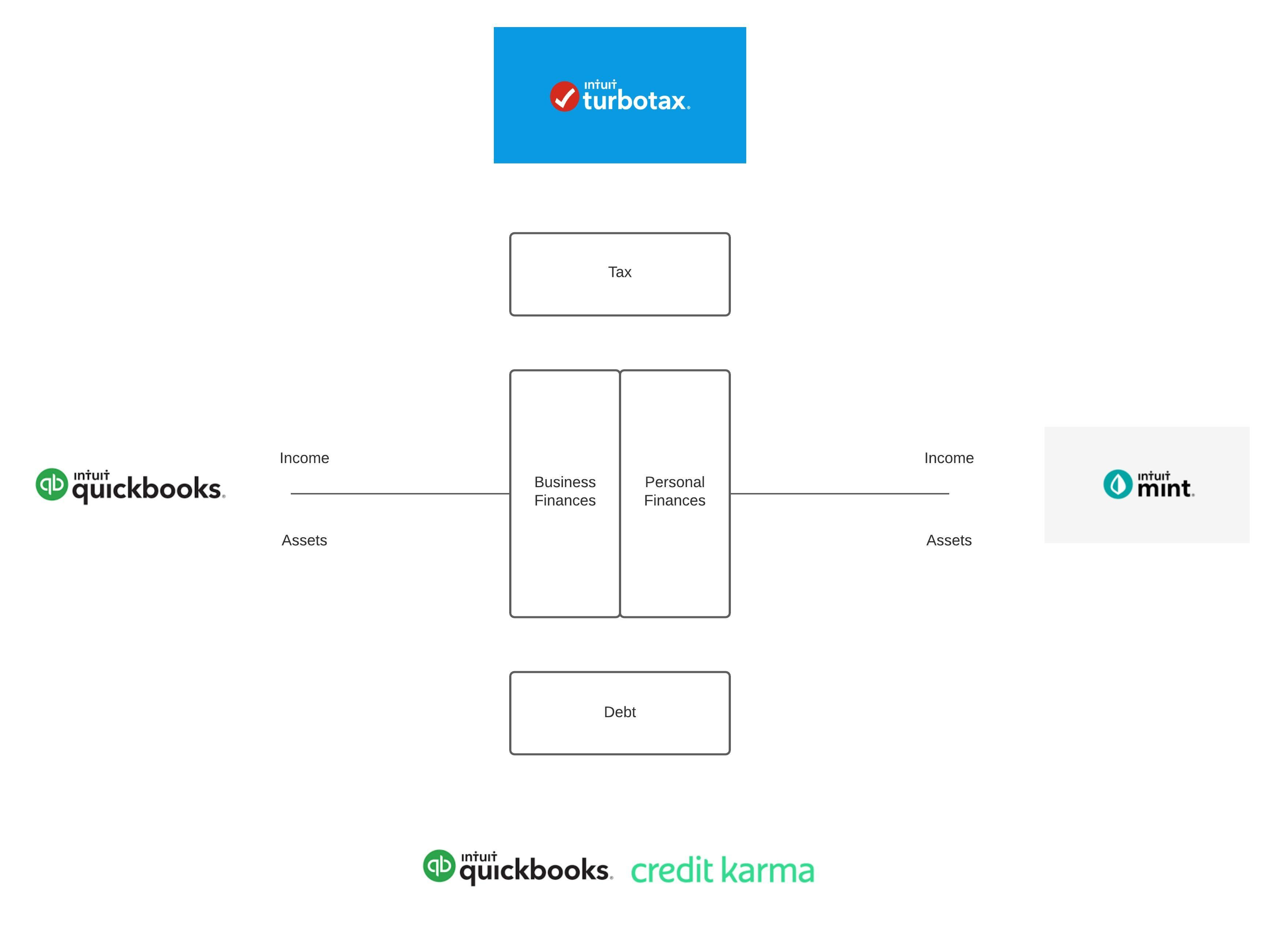

Take a look at the diagram below.

A typical small business owner has two facets of his financial life. Personal and business finances. In life and in business, finances can be broken up into two categories….income/expenses and assets/liability. Income/expenses from a business or personal financial standpoint also lead to taxes. Assets/Liabilities lead to debt/equity.

With Intuit’s pending acquisition of Credit Karma, Intuit will now have a suite of services which can provide a complete 360 degree view of the financial circumstances of small business owners everywhere.

Why is this important?

Growth strategies - Personal

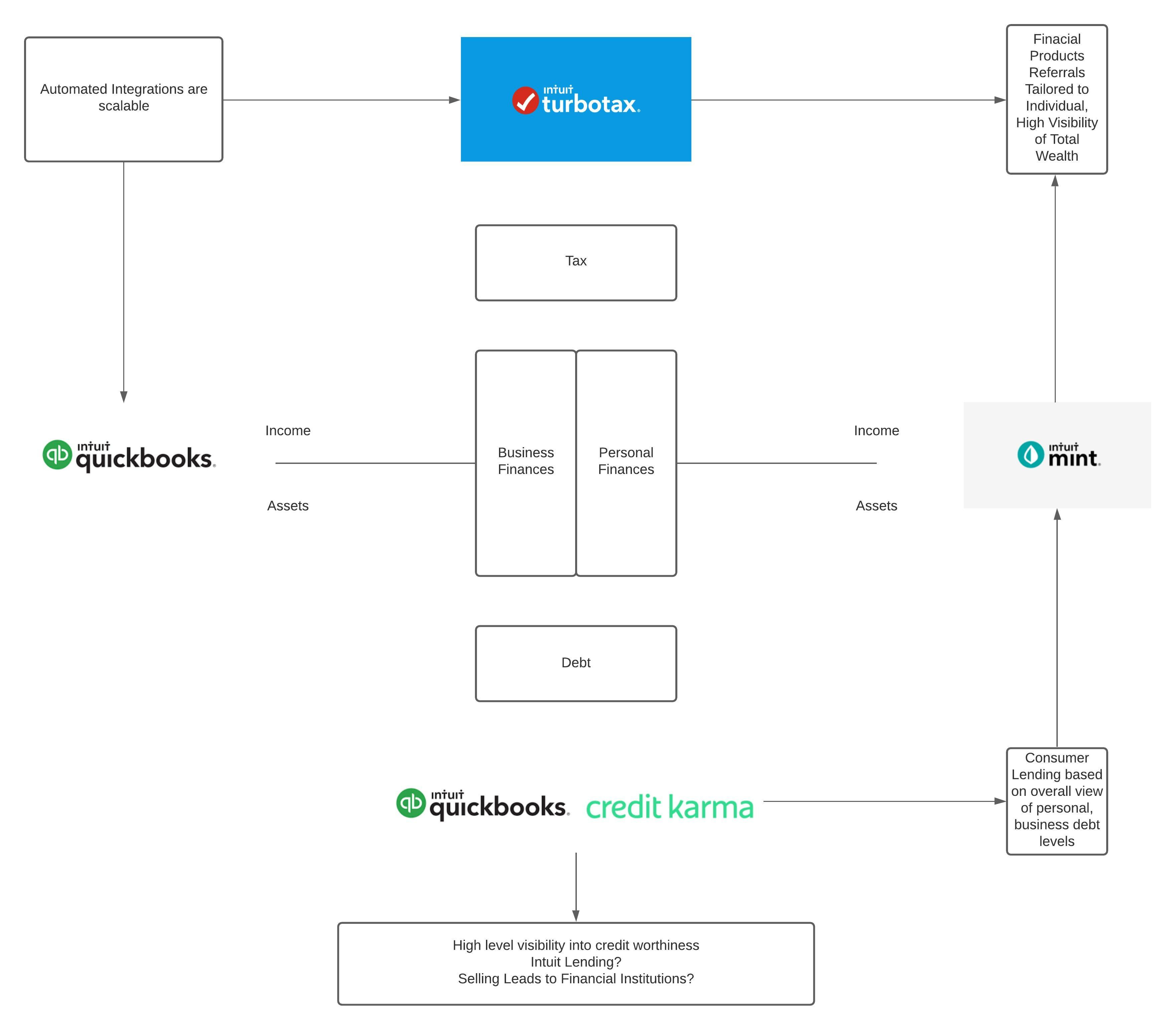

Take a look at the above image. It helps us to see how Intuit can use this data. On a consumer side, an overall view of financials such as taxes, income and credit history has significant potential for individual lending. Intuit could use these advantages in a number of scenarios.

Based on information gathered in the tax preparation process via TurboTax, and compared with information that’s linked into Mint via bank accounts, credit cards, monthly expenses; Intuit now has the ability to have a full view of what the accurate income of a person is. This is important for lenders to know when someone wants to purchase a home or a car or when applying a small business loan.

Adding Credit Karma to the mix will also give Intuit a view into credit worthiness and debt histories. If you think about the applications of machine learning, big data and AI, you can quickly see the power in this platform. Intuit will be able to analyze a person’s true credit worthiness on metrics that other companies will not have. A self reported level of income is worthless if the person who’s applying for a loan or credit card is not honest. Intuit won’t have that problem. They could decide to offer loans, credit cards, mortgages and other financial products with a high degree of certainty. They could even incentivize users of all 3 products by offering package discounts, much like an insurance may bundle home, auto and life at a better rate.

Or they could simply choose to sell a credit worthiness ratings to the bank with a highly accurate overview of a person’s true credit worthiness.

Growth strategies - Business

Up until this point we’ve focused on the personal side of Intuit’s offerings. However the true growth engine of Intuit will be and has been Quickbooks. Quickbooks is an essential software for many small businesses. Now each and every day thanks to the gig economy more and more Americans are opening up micro and small businesses. Because of the pandemic these businesses are in a greater need for loans than ever before.

Most banks do not want to lend on unsecured assets. They prefer mortgages or car loans (with a higher interest rate than other lenders) due to the risk profiles of these type of loans (asset secured). Thus it’s becoming more and more difficult for small businesses to obtain a loan. Regional banks may be more willing to do so, but even then the most common source of funding for a business is through friends and family.

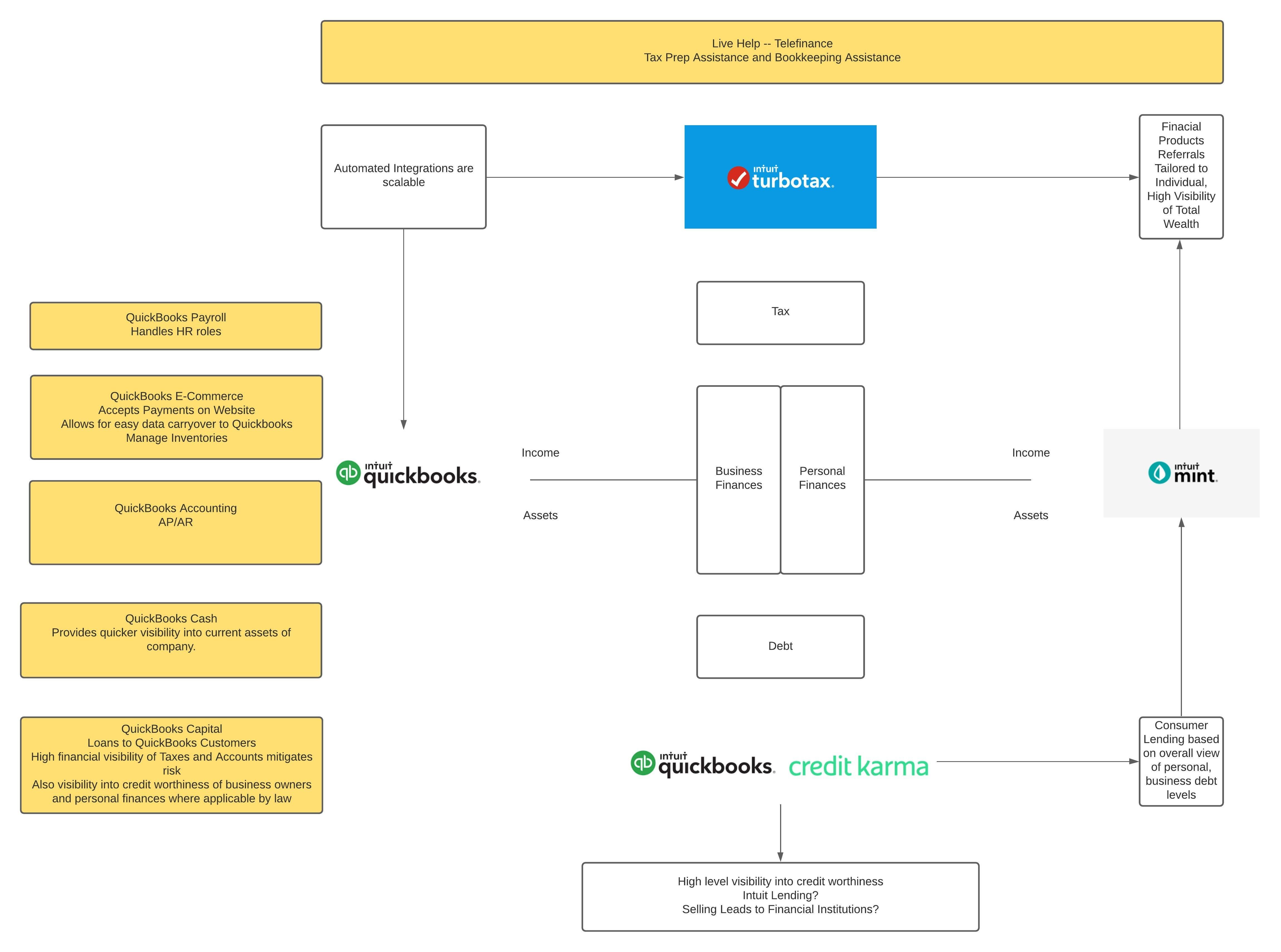

Intuit’s platform gives them a strategic advantage. They have access to data about so many businesses along with data to the finances, tax records and credit history of loan applicants. Think about how precise they will be able to calculate whether a loan is worth funding based on all of these data points. However Quickbooks is expanding beyond simply a bookkeeping software. See image below.

Quickbooks is now offering lending solutions, banking solutions, AP, AR, Payroll, E-Commerce Payments, Inventory Management, Live Help for Tax Prep Assistance and Bookkeeping Assistance.

Think of the opportunities that having all of these offerings opens to Intuit. Right now Quickbooks is seen as mostly a small business accounting platform. However consider where business and technology is right now. Most businesses now pay bills and invoices electronically either via a credit card or via online bill pay services.

Quickbooks has been designed to integrate with most platforms to automate as many steps of this process as possible. With modern technology a significant % of the AP/AR, Bookkeeping, Payroll and other essential business functions is now fully or mostly automated. This is the link which will allow Quickbooks and Intuit to take the next big step in it’s growth trajectory.

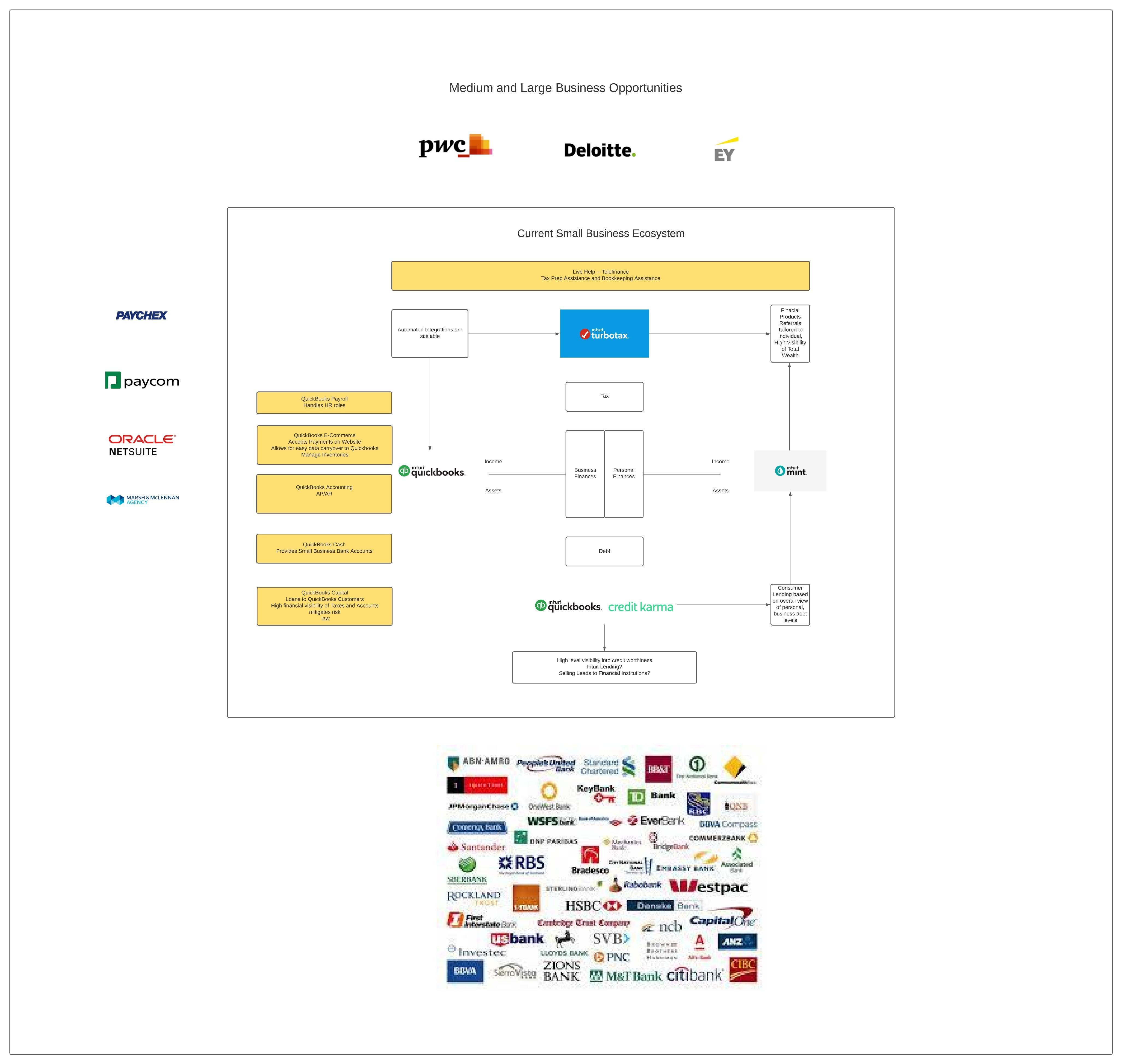

If you look at the above image, you’ll see some large name companies like Paychex, Paycom, Netsuite, PWC, Deloitte and a host of financial services companies. As Quickbooks continues to expand it’s omnichannel business service platform to include banking, lending, payroll, live tax assistance, live bookkeeping assistance, inventory, e-commerce and more; what’s to stop Intuit from starting to take market shares for entrenched players who only have 1 offering?

If Intuit can go to a medium sized business that currently uses Paycom for HR, Netsuite for Inventory, Wells Fargo for Banking and PWC for accounting; and they can say hey switch to Intuit, we’ll offer you all of these services and we can do it at a fraction of the cost with data and automation, why would a business say no? It simplifies their entire operating structure and provides meaningful value.

Valuation

All of this means nothing if Intuit isn’t trading at a fair value. Let’s look at the key components of it’s business and see if we can establish a meaningful valuation.

Intuit currently trades at an 89B dollar market cap. It’s earned 7.6B in revenues over the twelve trailing months or a valuation of 11x Sales and has a forward PE of about 40. It’s revenues increased about 14% annually over the past 3 years, while it’s net income increased 23% over the same time frame.

Looking at some other companies in similar spaces as Intuit, Equifax is at a 20B market cap, has a forward PE of about 25, and a ratio of 5.4x Sales. H&R Block is at a 3B market cap, has a forward PE of about 5, and a ration of 1.1x Sales. Square is a platform that like QuickBooks offer’s a variety of solutions to small businesses. It currently trades at 15x sales, a forward P/E of 156 and has an 83B market cap. Paycom is a software based payroll and HR solutions provider. It trades at a 21B Market cap, has a forward P/E of about 84x and is trading at 27x sales. Discover a provider of financial products has a 20B market cap, is trading at 10x forward earnings and less than 2x sales.

This is a broad spectrum of companies in a wide variety of fields, at a wide variety of valuations. Intuit sits in the middle of the valuation spectrum. What is intriguing about Intuit however is that they have tentacles which are starting to reach into the fields of each of these businesses.

Takeaway

In looking at the company, it’s current valuation relative to the low interest rates the economy will have until 2023 and seeing it’s overall total addressable market, I see a pathway which could lead Intuit to a near 200B valuation. I see a case where the company will continue to grow 15 to 20% for the next 5 years as it innovates it’s platform to be a single software solution for small and medium businesses and then begins to expand those services toward larger businesses helping them to become leaner and more automated in their accounting, inventory, HR and financial processes.